Table Of Content

Ideally, you'll want to have a credit score of 740 or better if you're getting ready to buy a house, since this will help you get a good mortgage rate. But it's possible to buy a house with a much lower score, particularly if you get an FHA loan, which allows scores down to 580 or even 500 with a large down payment. It's important to point out that your credit score isn't the only factor that lenders consider during the underwriting process. Even with a strong score, a lack of income or employment history or a high debt-to-income ratio could cause your mortgage approval to fall through. This is your only choice if you’re borrowing above the conforming loan limits, and these loans are more common in expensive cities throughout the country. Most jumbo loan programs require a credit score of at least 700, although there may be programs with lower score limits if you can afford a higher interest rate and payment.

How mortgage lenders pull credit

A loan backed by the Federal Housing Administration (FHA) is often the only choice for borrowers with a credit score between 500 and 619. You’ll pay for FHA mortgage insurance that includes an upfront premium of 1.75% of your loan amount and annual mortgage insurance premiums ranging between 0.15% and 0.75%. However, unlike PMI, the premium percentage is the same regardless of your credit score. The example also assumes you earn $85,000 per year and have $750 per month in nonmortgage debt. To find out whether you can buy a house — and how much you’re approved to borrow — get pre-approved by a mortgage lender.

Raise Your FICO® Score Instantly with Experian Boost™

"If we suddenly switched off the state pension or significantly reduced it, people would be in trouble, so the government can’t do that. Over the next 50 years, Tom predicts the proportion of GDP the state spends on older people will increase from around 16% to 25%. Rocket Homes Real Estate LLC is committed to ensuring digital accessibility for individuals with disabilities. We are continuously working to improve the accessibility of our web experience for everyone, and we welcome feedback and accommodation requests. If you wish to report an issue or seek an accommodation, please contact us at

Jumbo Loans Minimum Credit Score: 700

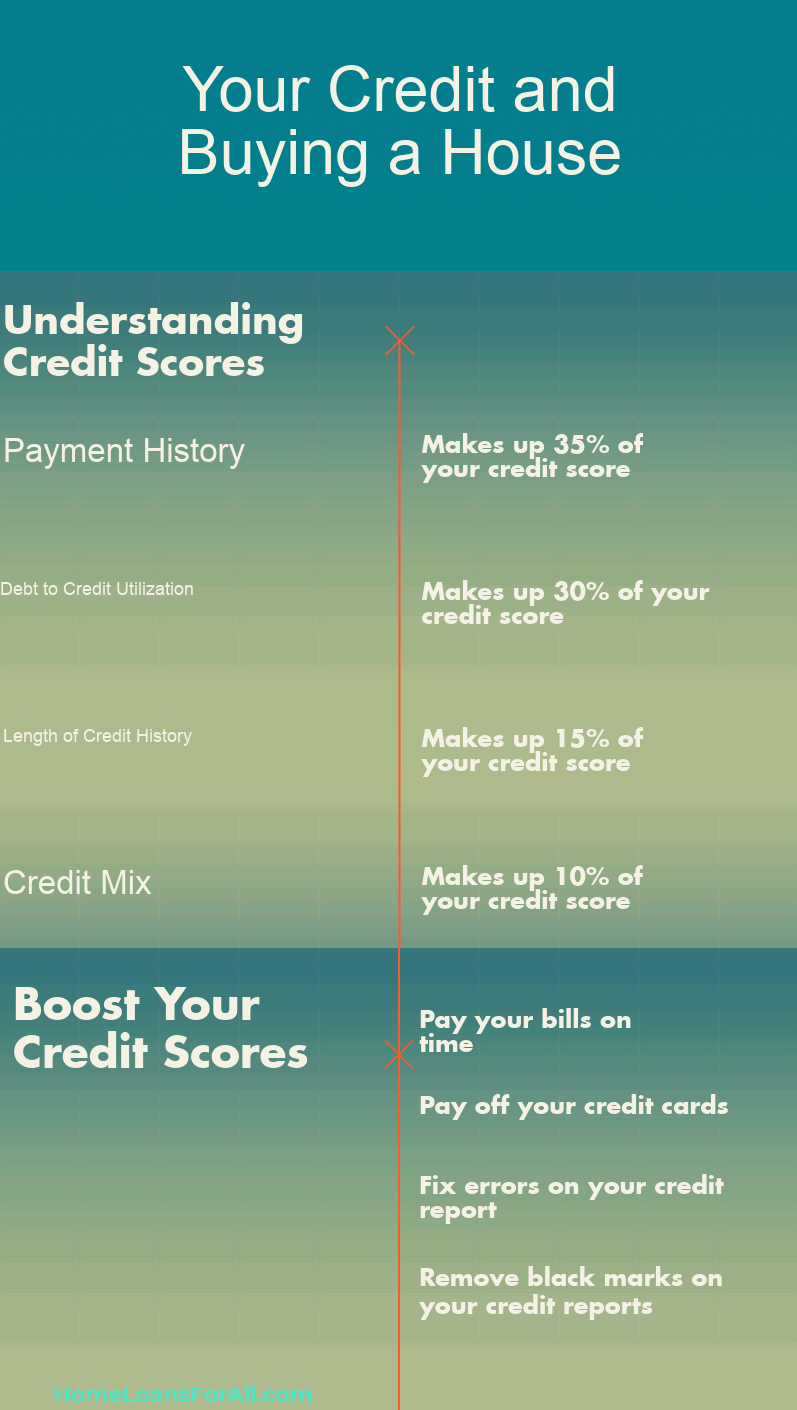

The more likely you are to pay your bills on time, based on your credit history, the lower your interest rate may be. With a less-than-stellar credit score, however, you may end up paying more. A credit score isn’t the only deciding factor on your mortgage application, but it’s a significant one. So when you’re house shopping, it’s important to know where your credit stands and how to use it to get the best mortgage rate possible. Be sure to make on-time payments on all your loans and credit cards.

The credit score needed to buy a house - Yahoo Finance

The credit score needed to buy a house.

Posted: Wed, 13 Mar 2024 07:00:00 GMT [source]

Surprisingly, some top-tier lenders specialize in assisting borrowers whose credit scores hover around or even dip below 600. Another appealing quality is that, unlike conventional loans, FHA-backed mortgages don’t carry risk-based pricing. Risk-based pricing is a fee added to loan applications with lower credit scores or other less-than-ideal traits.

The cost of bread, biscuits and beer could increase this year due to the impact of the unusually wet autumn and winter on UK harvests. Ottolenghi said he had "always been super eager to get our flavours onto people's dinner plates nationwide, not just in London, without having to cook it from scratch every single time". Waitrose is launching an exclusive range of products with popular chef Yotam Ottolenghi today. Staff at the UK's biggest airport are set to walk out during the early bank holiday in May, with their union warning planes could be "delayed, disrupted and grounded".

These loans often necessitate a 10–20% down payment, incorporating home equity as a key part of the borrowing strategy. FHA loans are known for allowing the lowest credit scores compared to other loan programs, accepting FICO scores of 580 and above, with only a 3.5% down payment required to buy a house. For an FHA loan, you may qualify with a credit score as low as 500 if you can provide a 10% down payment. For a conventional loan, often backed by Fannie Mae and Freddie Mac, a minimum score of 620 is typically required. Different lenders accept different LTV ranges, but it’s best if your ratio is 80% or lower.

This program also requires the buyer to meet certain income criteria and purchase a home in a designated rural area. It’s important to remember that while lenders have minimum credit score requirements, having a higher score can improve your chances of getting a better mortgage deal. Paying down your credit card balances also improves your credit utilization ratio, or the amount of money you spend compared to your total credit limit.

By following these proven steps, you can significantly improve your appeal to lenders and streamline your home buying process. Still, some home buyers can qualify for a home loan with a FICO score as low as 500, depending on the loan program. Uncover down payment assistance programs and down payment assistance grants that can ease the financial burden of a home purchase. Considering the example above, if you take out a $110,000 loan and put $40,000 down ($10,000 more than before), your LTV is now 0.73, or 73%. The loan-to-value ratio (LTV) is another factor used to determine how you qualify for a home loan. There are many ways to calculate a credit score, but the most sophisticated, well-known scoring models are the FICO®Score and VantageScore® models.

Additionally, borrowers with bad credit may have to go through a more in-depth underwriting process. However, nearly all loans follow this simple step-by-step process. Lenders look at your credit score, DTI, LTV, and assets together to assess your entire financial picture. You may fall short in one area, but can get approved if you are strong in others. For example, if you have a low credit score, you may be required to make a larger down payment, have a greater amount of cash reserves, and have a lower DTI.

Tracy says there's currently a surge in people wanting to buy "mid century" furniture, which is dated to roughly 1945 to 1965 and typically uses clean lines and has a timeless feel. While my hot pink Gameboy Micro is lost to the void of time (or a cardboard box somewhere in my mum's house), other versions of it are selling on eBay for £100 or more. The average price paid for comprehensive motor insurance rose 1% in the first quarter of the year, according to industry data indicating an easing in the steep rises seen last year. Strikes tend to mean services on lines where members are participating are extremely affected or cancelled entirely, whereas overtime bans often lead to reduced services. Overtime bans, an action short of a strike, means some services may not be running or may be reduced as drivers refuse to work their rest days.

It’s important to know your credit score and exactly what’s on your credit report. Because home-buying may be more complicated when you have bad credit, there are some additional steps you can take to increase your chances of approval. Washington, D.C., Credit Karma members had the highest average mortgage balance at $452,712. Of course, the offers on our platform don’t represent all financial products out there, but our goal is to show you as many great options as we can.

Today, Zillow Home Loans helps would-be homeowners who are seeking financing for primary homes, vacation homes and investment properties. Existing homeowners who are looking for refinancing options may find solutions from Zillow Home Loans, as well. Plus, you're also taking on untold unpredictable expenses -- if something breaks, it'll be on you to pay to fix it. Owing less money to other creditors and having more space in your budget can help immensely. The table below summarizes generational differences among Credit Karma members with mortgages. This might indicate a general decline of credit health across all consumers over the last two years.

Maybe you prefer paying cash over using credit; maybe you’re too young to have a credit history; or perhaps you carry high balances. Your credit score is just one element that goes into a lender’s approval of your mortgage. Here are some other personal factors that lenders consider when qualifying you for a mortgage. Having a higher credit score can save you thousands in interest payments over the life of a mortgage — and help with insurance premiums, too. For more people, their credit score is one of the most important factors in determining whether or not they can buy a home. Lenders lean heavily on your score — which can range from 300 on the low end all the way up to 850 — to decide whether to approve you and what interest rate to offer.

You’ll typically need a credit score of 620 to finance a home purchase. However, some lenders may offer mortgage loans to borrowers with scores as low as 500. Buying a house with bad credit is challenging, but not impossible. Certain types of loans, like FHA loans, are designed for borrowers with lower credit scores. It’s important to first review your credit report, which you can obtain for free from annualcreditreport.com, to understand your financial standing.